Understanding DSCR Loan Rates

A Debt Service Coverage Ratio (DSCR) loan is a financing product that flips traditional lending on its head, focusing on the property’s cash flow instead of your personal tax returns. This is great news for investors who might have complex financials and won’t qualify for a traditional loan.

However, because these loans are a type of non-qualified mortgage (Non-QM), they are priced differently—and often higher—than a conventional loan. The interest rate you get can make or break your investment’s profitability.

So, what truly moves the needle on your DSCR loan rate?

It all boils down to risk.

Your lender is essentially asking, “How risky is this investment, and how reliable is the person running it?” Let’s pull back the curtain and look at the four major factors that will determine where your final DSCR interest rate lands plus actionable items to improve your DSCR loan rate.

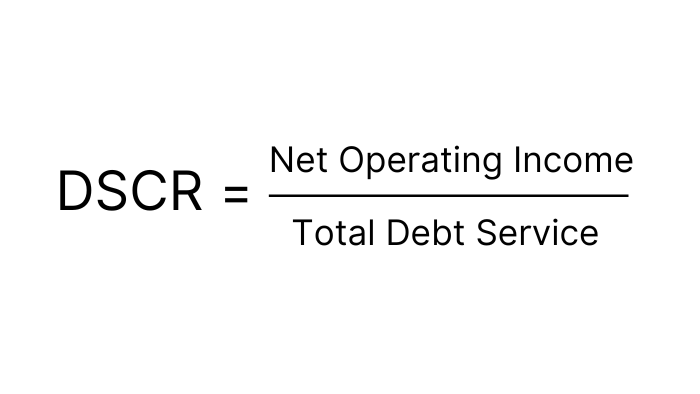

1. The Debt Service Coverage Ratio (DSCR) Itself: The King of the Rate

This factor is the most important one, and it’s right there in the name. The DSCR is a measure of the property’s annual rental income (minus operating expenses) divided by the total annual debt service (Principal, Interest, Taxes, Insurance, and sometimes HOA).

Think of the DSCR as your property’s security blanket. A higher DSCR means a thicker, warmer blanket—and a happy, less-stressed lender who will reward you with a lower interest rate.

- The Sweet Spot (1.25x and Up): Most lenders prefer to see a DSCR of 1.25x or higher. This means the property generates $1.25 in income for every $1.00 of mortgage debt. Investors who can consistently hit this range often qualify for the most competitive pricing tiers.

- Preferred Pricing (1.40x and Up): If your property’s cash flow is exceptional and you can hit $1.40 in income for every $1.00 of debt, you may unlock the absolute best rate the lender offers, depending on other factors we will discuss further below.

- The Risky Zone (1.0x or Lower): A DSCR of 1.0x means the property income just barely covers the debt. Anything below 1.0x is considered “negative cash flow.” While some lenders offer “No Ratio” or “Sub-1.0x” programs, be prepared to face tighter credit score requirements and pay a substantial premium —we’re talking significantly higher interest rates, more points, and a larger down payment—to offset the increased risk.

Your Action Plan: Before you even apply, stress-test your rental projections to see where your property’s DSCR falls. A difference of 0.1 in the ratio could translate to a quarter-point difference in your rate.

2. Borrower’s Credit Score: Your Personal Guarantee

While the DSCR loan shifts the focus from your personal income, it never ignores your personal credit history. Your credit score still serves as a good measure of your general financial reliability. Are you the kind of borrower who pays on time, every time? Your score answers that question.

The lender knows that if the property runs into a temporary snag (like a sudden vacancy or a major repair), the money to cover the mortgage will have to come from you.

- The Gold Standard (740+): A FICO score in the mid-700s or higher is your ticket to the best DSCR rates. It tells the lender that you are a highly responsible borrower with a proven history of managing debt.

- The Minimum Barrier (660-680): Most DSCR loan programs require a minimum credit score, often around 660 or 680. If you are at this baseline, you will qualify, but you should expect an interest rate that is noticeably higher than a top-tier borrower.

- The Score-Rate Trade-off: The interest rate tiers for DSCR loans are heavily structured around your credit score. Don’t be surprised if moving from a 700 score to a 720 score drops your rate by 0.125% or 0.25%.

Your Action Plan: If you are a month or two out from applying, focus on paying down high-interest debt and correcting any credit report errors. A small boost in your score can save you tens of thousands of dollars over the life of the loan.

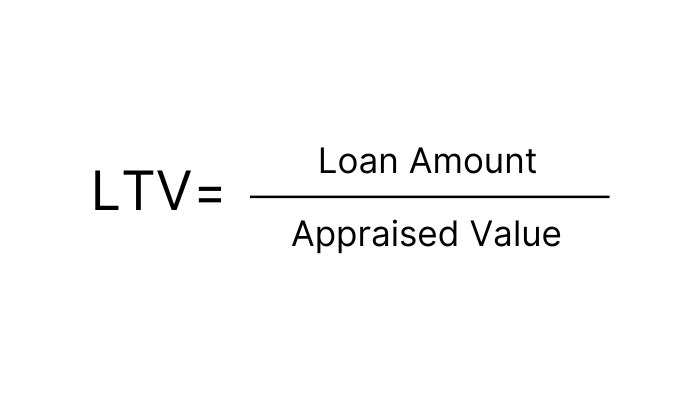

3. Loan-to-Value (LTV) Ratio: Skin in the Game

The Loan-to-Value (LTV) ratio measures the size of the loan relative to the property’s appraised value. It’s the lender’s measure of how much “skin you have in the game.”

- Lower LTV (Better Rate): A low LTV, achieved by making a larger down payment, is always viewed favorably. For instance, putting 30% to 35% down (LTV of 70% or 65%) significantly reduces the lender’s exposure to risk, as they have a larger equity cushion in the event of a default. This typically earns you the most favorable rate.

- Higher LTV (Higher Rate): If you are leveraging more capital by putting the minimum down (often 20% to 25%, or LTV of 80% to 75%), the lender will charge a higher rate to compensate for the slimmer equity cushion.

Your Action Plan: Consider your real estate investment strategy carefully. If your goal is to maximize your portfolio growth by preserving cash reserves, you might tolerate a higher rate for a higher LTV. If your goal is pure cash flow maximization on this single property, a larger down payment for a lower rate is the smarter move.

4. Property Type and Use: Understanding the Risk Landscape

Finally, the nature of the investment property itself will impact the rate. Lenders assign different risk profiles to different types of real estate, which is reflected in their pricing.

- Single-Family Rentals (SFR) and Standard Long-Term Leases: These are generally considered the most stable investment and often receive the most competitive rates. Lenders view a 12-month lease on a 4-bedroom house as highly predictable income.

- Short-Term Rentals (STR/Airbnb): Properties intended for short-term rentals carry more income volatility (seasonal swings, market saturation, local regulation risk). Because of this, lenders will often charge a small premium on the interest rate, and they may require a higher minimum DSCR to prove the property can generate sufficient income even during slower seasons.

- Small Multi-Family (2-4 Units): While generally viewed as stable, these properties have slightly more complex operations and may see a rate that sits just above the top-tier SFR pricing.

Your Action Item: If financing a Short-Term Rental, proactively provide comprehensive documentation such as historical revenue reports (if refinancing) or detailed, third-party AirBNB/rental projections (if purchasing). For multi-family units, ensure your expense documentation is meticulously separated by unit. By clearly and confidently presenting the property’s profitability and income stability, you help the lender view your unique asset as lower risk, which can mitigate rate increases tied to its use.

Get The Best DSCR Loan Rate

The beauty of the DSCR loan is that you, the investor, have tremendous influence over your final rate. It’s not a mystery—it’s a formula. By strategically maximizing your property’s cash flow (to boost the DSCR), maintaining a strong credit profile, and optimizing your down payment (to lower the LTV), you can position yourself to secure financing on the best possible terms.

Don’t leave your rate to chance. Start by understanding your metrics and then work with a partner who specializes in navigating this intricate Non-QM market.

Ready to Maximize Your Investment Portfolio?

Securing the optimal DSCR loan rate is the first step toward long-term real estate success.

At GL&L Holdings, we specialize in non-qualified mortgages for real estate investors, offering competitive rates tailored to your unique investment strategy and portfolio goals. Stop settling for generic, high-cost investment loans.

Get a personalized DSCR loan quote today and find out exactly how much you can save!